File:Covariance_trends.svg · Wikimedia Commons · See Wikimedia Commons

covariance

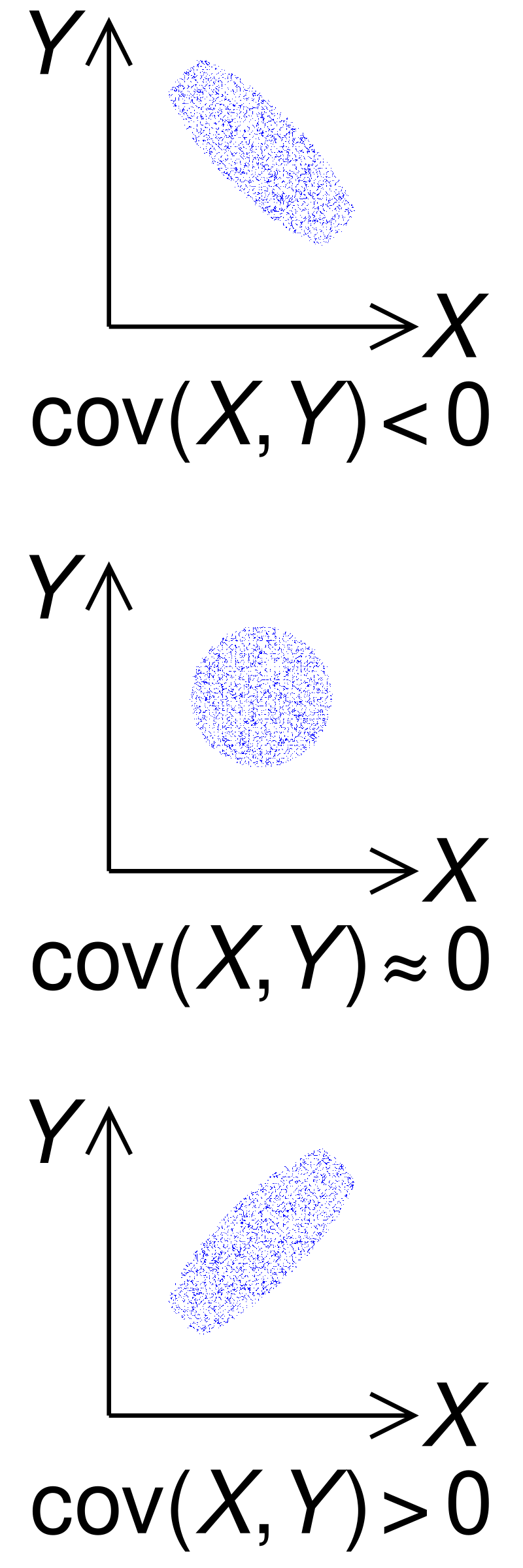

Sign in to savethumb|upright|The sign of the covariance of two random variables X and Y

Wikidata facts

Show 1 more fact

- Stack Exchange tag

- stackoverflow.com/tags/covariance

Sources (3)

via Wikidata · CC0

~23 min read

Article

27 sectionsContents

- Definition

- Complex random variables

- Discrete random variables

- Examples

- Properties

- Covariance with itself

- Covariance of linear combinations

- Hoeffding's covariance identity

- Uncorrelatedness and independence

- Relationship to inner products

- Calculating the sample covariance

- Generalizations

- Auto-covariance matrix of real random vectors

- Cross-covariance matrix of real random vectors

- Cross-covariance sesquilinear form of random vectors in a real or complex Hilbert space

- Numerical computation

- Comments

- Applications

- Genetics and molecular biology

- Financial economics

- Meteorological and oceanographic data assimilation

- Micrometeorology

- Signal processing

- Correlation

- Principal component analysis

- See also

- References

thumb|upright|The sign of the covariance of two random variables X and Y

In probability theory and statistics, covariance is a measure of the joint variability of two random variables. The sign of the covariance shows the tendency in the linear relationship between the variables. Covariance is positive when variables tend to show similar behavior and negative when variables tend to show opposite behavior. The magnitude of the covariance is the geometric mean of the variances that are shared for the two random variables, where a larger magnitude means two variables more strongly depend on each other.